When you apply for a new mortgage, the lender will evaluate your creditworthiness to determine whether to approve your application and what terms and interest rate to offer you. Your existing debt can affect your creditworthiness in several ways:

When you apply for a new mortgage, the lender will evaluate your creditworthiness to determine whether to approve your application and what terms and interest rate to offer you. Your existing debt can affect your creditworthiness in several ways:

Debt-to-income ratio (DTI): Your DTI ratio is the percentage of your monthly income that goes towards paying off debt. Lenders typically want to see a DTI ratio of 43% or less, meaning your debt payments don’t exceed 43% of your gross monthly income. If your existing debt is high, your DTI ratio will be high, and lenders may view you as a riskier borrower. This can make it more difficult to qualify for a new mortgage or result in a higher interest rate.

Credit score: Your credit score is a numerical representation of your creditworthiness, based on your credit history. If you have existing debt and have been making late payments or defaulting on payments, your credit score may have taken a hit. This can make it more difficult to qualify for a new mortgage or result in a higher interest rate.

Payment history: Your payment history is a record of how consistently you have made payments on your existing debt. If you have a history of late payments or defaulting on payments, this can signal to lenders that you may be a riskier borrower, which can make it more difficult to qualify for a new mortgage or result in a higher interest rate.

Available funds for down payment: If you have existing debt, you may not have as much money available for a down payment on a new mortgage. This can make it more difficult to qualify for a new mortgage or result in a higher interest rate.

Overall debt load: Lenders will also consider your overall debt load when evaluating your creditworthiness. If your existing debt is high relative to your income and assets, this can make it more difficult to qualify for a new mortgage or result in a higher interest rate.

In summary, your existing debt can affect your ability to qualify for a new mortgage by increasing your DTI ratio, lowering your credit score, affecting your payment history, limiting your funds for a down payment, and increasing your overall debt load.

It’s important to manage your debt carefully and maintain a good credit score if you’re planning to apply for a new mortgage. By evaluating the following and staying on track, you can ensure that you’re ready for the financial responsibilities of a mortgage and can make an informed decision about homeownership.

Mortgage points, also known as discount points or origination points, are fees paid by borrowers at closing to reduce the interest rate on their mortgage loan. Each point typically costs 1% of the total loan amount and can lower the interest rate by anywhere from 0.125% to 0.25%.

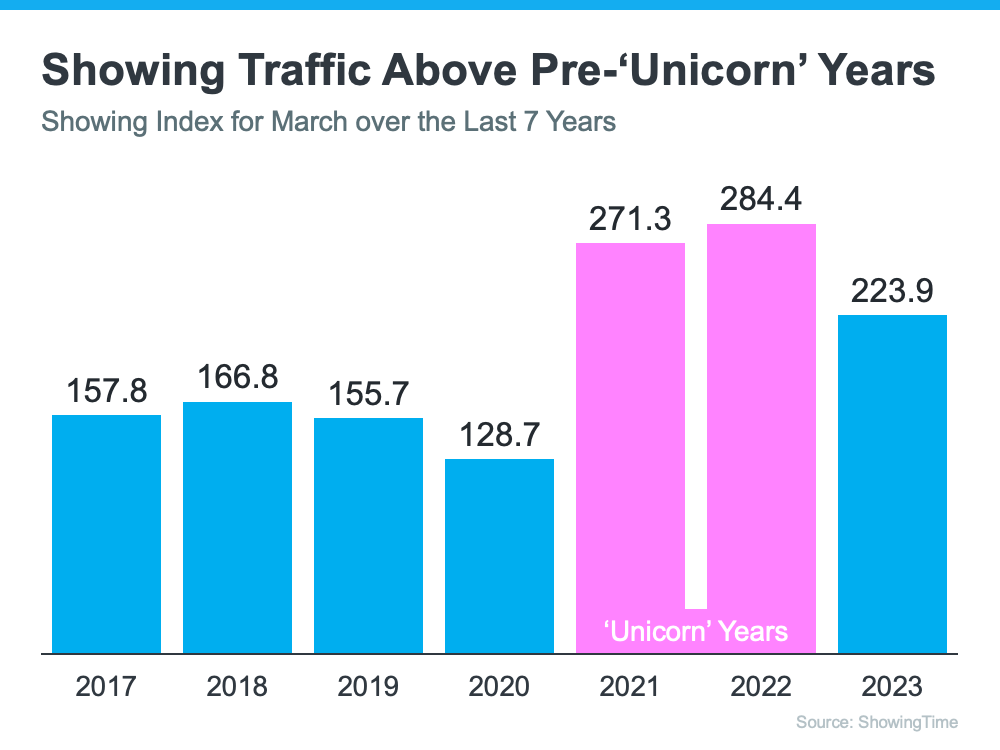

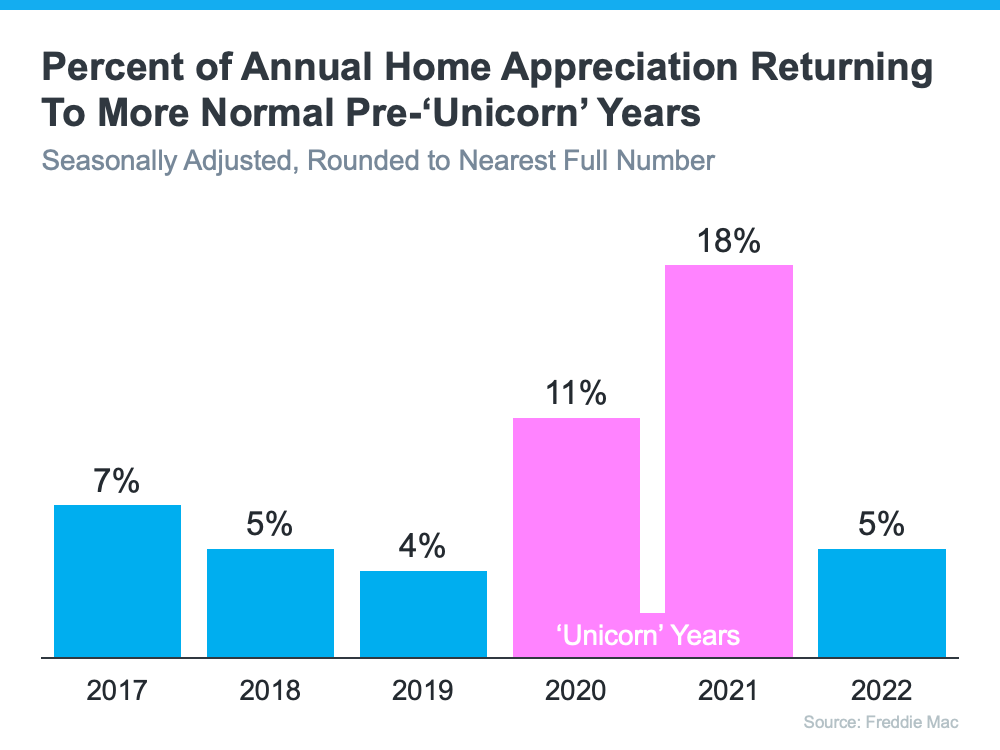

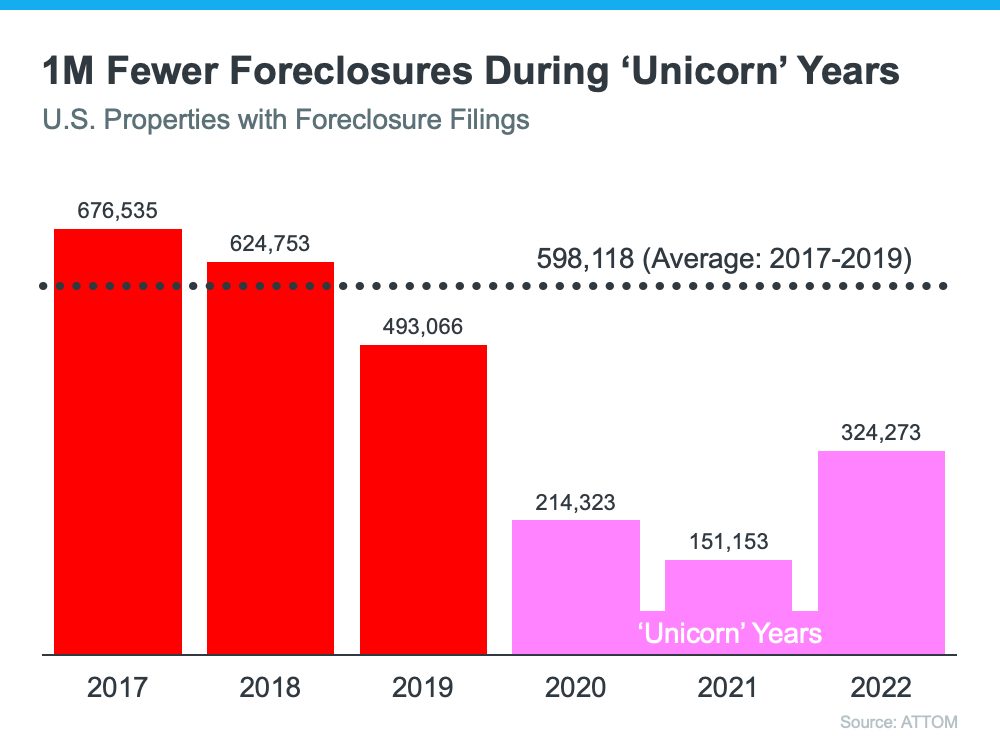

Mortgage points, also known as discount points or origination points, are fees paid by borrowers at closing to reduce the interest rate on their mortgage loan. Each point typically costs 1% of the total loan amount and can lower the interest rate by anywhere from 0.125% to 0.25%. Comparing real estate metrics from one year to another can be challenging in a normal housing market. That’s due to possible variability in the market making the comparison less meaningful or accurate. Unpredictable events can have a significant impact on the circumstances and outcomes being compared.

Comparing real estate metrics from one year to another can be challenging in a normal housing market. That’s due to possible variability in the market making the comparison less meaningful or accurate. Unpredictable events can have a significant impact on the circumstances and outcomes being compared.