There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

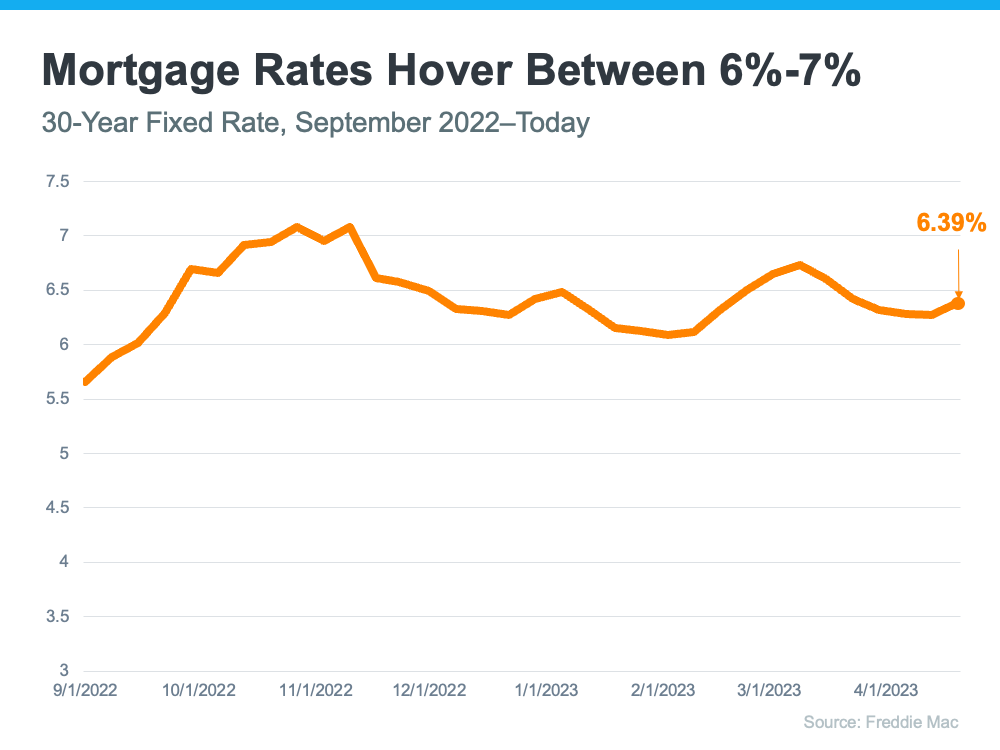

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

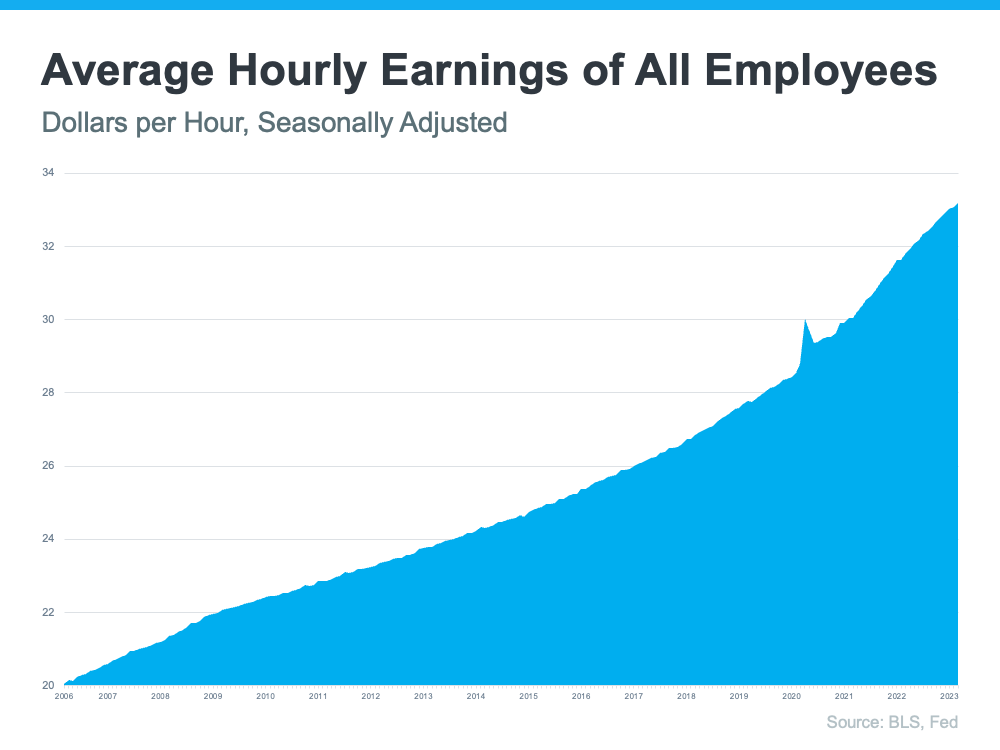

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage since you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability comes down to a combination of rates, prices, and wages. If you have questions or want to learn more, reach out to a real estate professional who can explain what’s happening locally and how these factors work together.

Bottom Line

If you’re planning to buy a home, knowing the key factors that impact affordability is important so you can make an informed decision. To stay up to date on the latest on each, let’s connect today: Bob 612 868 5500 or Bob@mnresteam.com

Are you interested in refinancing your mortgage? There are a variety of reasons why you might want to refinance your home loan. For example, you might want to secure a lower interest rate, or you may want to reduce your monthly payment. You might even want to tap into the equity you have in your home for some quick cash. There are different loan options available, so you need to think carefully about which one is best for your needs.

Are you interested in refinancing your mortgage? There are a variety of reasons why you might want to refinance your home loan. For example, you might want to secure a lower interest rate, or you may want to reduce your monthly payment. You might even want to tap into the equity you have in your home for some quick cash. There are different loan options available, so you need to think carefully about which one is best for your needs. How to Get Rid of PMI?

How to Get Rid of PMI?